As we discussed earlier (article – Cryptoregulation in the ADGM free financial zone), ADGM remains to be a leading crypto-regulator in the UAE. This time, we will shed a light on regulatory approaches towards the crypto token offering in this special economic zone and discuss the classifications set out by the governing rules in the zone.

ICO requirements

As the competent regulator in ADGM, the Financial Services Regulatory Authority (“FSRA”) of the Abu Dhabi Global Market (ADGM), in October 2017, the FSRA issued a guidance applicable to those considering offering virtual assets. The guide has been updated for several times ( in June 2018 and May 2019, in February 2020 and 2021) subject to regulation in accordance with the Financial services and markets regulations (hereinafter: “FSMR”). This may be the case when the FSRA determines that the tokens exhibit the characteristics of securities. In this case, the FSRA considers virtual assets to be digital securities and an ICO must comply with the FSMR if it is offered within ADGM or outside of the ADGM. Accordingly, if an ICO is issued overseas but offered to the public at the ADGM, a decision from the FSRA must be sought, unless purchasers located at the ADGM are excluded from participation.

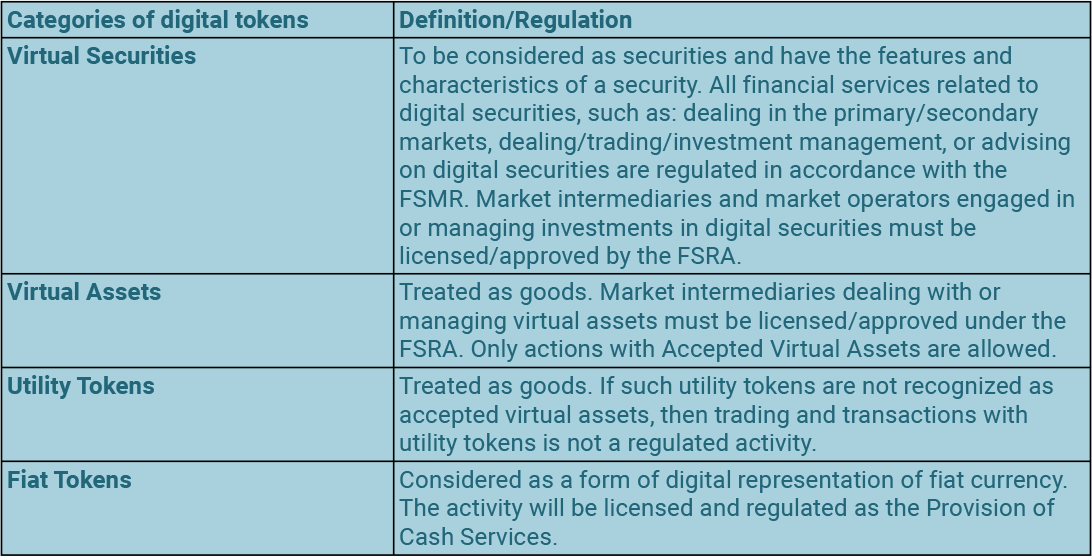

FSMR divides virtual coins and tokens into FSRA regulated digital assets on the one hand, which includes virtual assets (such as non-fiat virtual currencies including Bitcoin and Ethereum), digital securities, fiat tokens (fully backed by fiat)) and derivatives and funds (i.e. derivatives for any digital assets and collective investment funds investing in digital assets) and other digital tokens. However, only utility tokens remain unregulated.

The FSMR defines a virtual asset as a digital representation of value that can be digitally traded and functions as a medium of exchange, unit of account, or store of value, or all three, but does not have legal tender status in any jurisdiction. From a regulatory policy perspective, the FSRA treats virtual assets as commodities and therefore not as certain investments under the FSMR. Derivative virtual assets are treated as commodity derivatives and therefore as certain investments under the FSMR. While not all virtual assets are defined as investments, any market operator, intermediary or custodian dealing with virtual assets must be approved by the FSRA as a Financial Services Authorization Holder for applicable regulated activities.

Digital Securities Guidance

In addition, the FSRA’s decision to treat a token as a security gives rise to prospectus obligations under Section 61 of the FSMR, other obligations under Chapter 4 of the FSMR Market Rules, and AML and KYC requirements. The normal prospectus exceptions may apply if the offer is made only to professional clients (as defined in the FSMR) or to less than 50 individuals in any 12-month period, or when the consideration to be paid by one individual for the purchase of tokens is at least $100,000 United States (EUR 91642). In its latest guidance on digital securities, the FSRA suggests that issuers of digital securities must fully consider the context of both the primary and secondary markets. This includes an obligation for the issuer to also seek admission of digital securities to trading on multilateral trading venues and recognized investment exchanges operated by ADGM due to the incomplete integration of the primary and secondary markets for digital securities.

Classification as a digital security also requires that market intermediaries or operators such as virtual currency exchanges that trade these tokens are regulated as:

- holders of permits for financial services;

- recognized investment exchanges;

- recognized clearing houses.

It is important to note that the FSRA does not currently provide permission for the secondary market to list digital securities issued outside the ADGM.

Moreover, the FSRA may consider tokens used by firms to create an investment fund on the blockchain as units of a collective investment fund (as defined in section 106 of the FSMR) to which the rules of the ADGM fund apply. This classification also gives rise to extensive regulatory requirements.

If the token to be issued is a stablecoin, it can only be issued and offered within the ADGM, where it is 1:1 backed by fiat currency and will then be characterized as a fiat token. Its issuer is considered a money services business that must be authorized to provide financial services for a regulated money services business. Only in cases where the FSMR does not consider digital tokens to be digital securities, fiat tokens, or derivatives can an ICO fall outside the scope of ADGM. The FSRA ICO Guidelines encourage the industry to develop voluntary best practices for such ICOs.

TOKEN CLASSIFICATION AS PER CRYPTO REGS

Paragraph 10 of the Regulations on the Regulation of Activities with Virtual Assets in the ADGM provides a classification of tokens, which is displayed in Table No. 1:

Тable №1

Stablecoins

According to Article 162 of the ADGM’s Virtual Asset Regulation, a stablecoin is a type of blockchain-based fiat token that is valued against a base fiat currency. The key feature of a stablecoin is that it should have less volatility than other virtual assets, which allows it to work as a value transfer in the virtual asset ecosystem, including as part of a trading pair on the MTF (Multilateral Trading Facilities).

Demand for stablecoins in the virtual asset markets continues to grow as many participants look for a safe store of value. Demand has also increased as a result of the general inability to convert virtual assets into fiat currencies. In addition, some stablecoins are designed more to function as digital currencies within the digital economy.

The FSRA’s position on stablecoins is as follows:

- only allow stablecoins that are a fully backed 1:1 fiat token, backed only by the same fiat currency it is intended to be tokenized;

- fiat tokens should be considered as a mechanism for storing value (for example, electronic money);

- issuers of fiat backed tokens for the purpose of facilitating or making payments are treated as businesses providing money services. In addition to the need to have an FSP for a regulated money services business.

The comprehensive regulatory framework and clarifications from the ADGM authorities have made the Free Zone even more secure for Virtual Asset service providers to do business in more favorable conditions.

The content of this article is intended to provide a general guide to the subject matter, not be considered as a legal consultation.