Despite the growing nature of virtual currencies - being the digital representations of value and utilities as a medium of exchange, they are still not officially considered to be legal tender in many countries across the globe, including in Poland.

But that vague regulatory schemes didn’t stop their extensive use, so the officials are trying to address the legal gaps to minimize the risks and are regarding them as a potential means to increase central government revenue by introducing relevant taxes.

In 2019, the legislative body eliminated doubts by introducing statutory measures to address the taxation regime of profits made from digital currencies. The article analyses the amended legislative acts, specifically Personal Income Tax Act (hereinafter “PIT” Act); Tax on civil law transactions Act (hereinafter: “PCC Act”) and Tax on goods and services Act (hereinafter: – “VAT Act”) and tax implication over transactions using cryptocurrencies.;

Personal Income Tax

Pursuant to article 10 of the PIT act, revenues obtained from trading cryptocurrencies are classified as the source of revenues from:

cash capitals and property rights, including the sale of property rights;

non-agricultural economic activity: if the cryptocurrency is traded as part of an activity that meets certain conditions, including: it is of a profit-making nature, it is conducted on its own behalf by the taxpayer, in an organized and continuous manner (and the conditions specified in Art.5b (1) of the PIT Act are not met).

selling cryptocurrencies (converting cryptocurrencies into traditional currencies, e.g. zlotys (PLN), euro (EUR), US dollar (USD),

exchanging cryptocurrency for another cryptocurrency, for a good or a service. The exchange of cryptocurrencies should be treated as a form of its sale for consideration, similar to the exchange of any other property rights, e.g. receivables.

The income from the property rights referred to in art. 18 of the PIT Act arises when money (traditional currency), other cryptocurrency, goods or services are provided to the taxpayer. While the income from the business activities is considered to be amounts due, even if they have not been actually received. At the same time, the date on which the income from business activity arises is the date of sale of the property right – i.e. the date of sale or exchange of a given cryptocurrency – no later than the date of invoice or payment of the amount due.

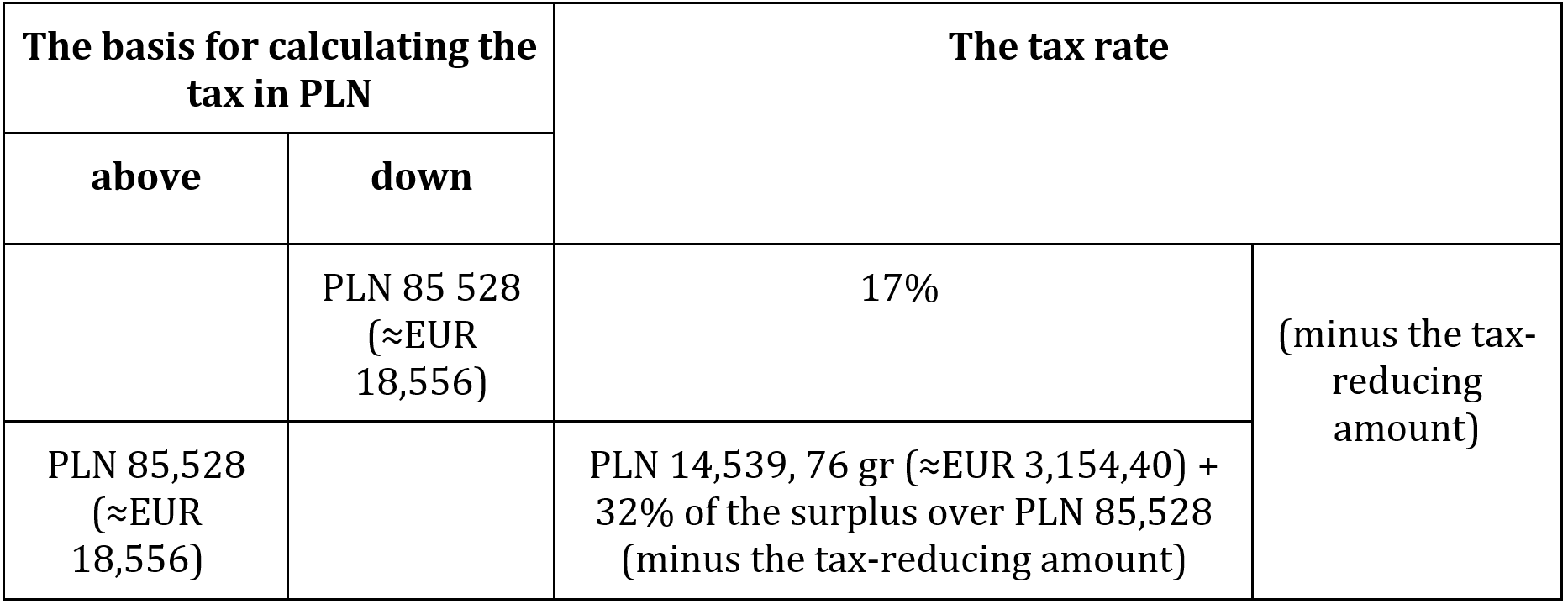

Income tax rates

Income from cryptocurrency turnover qualifies for:

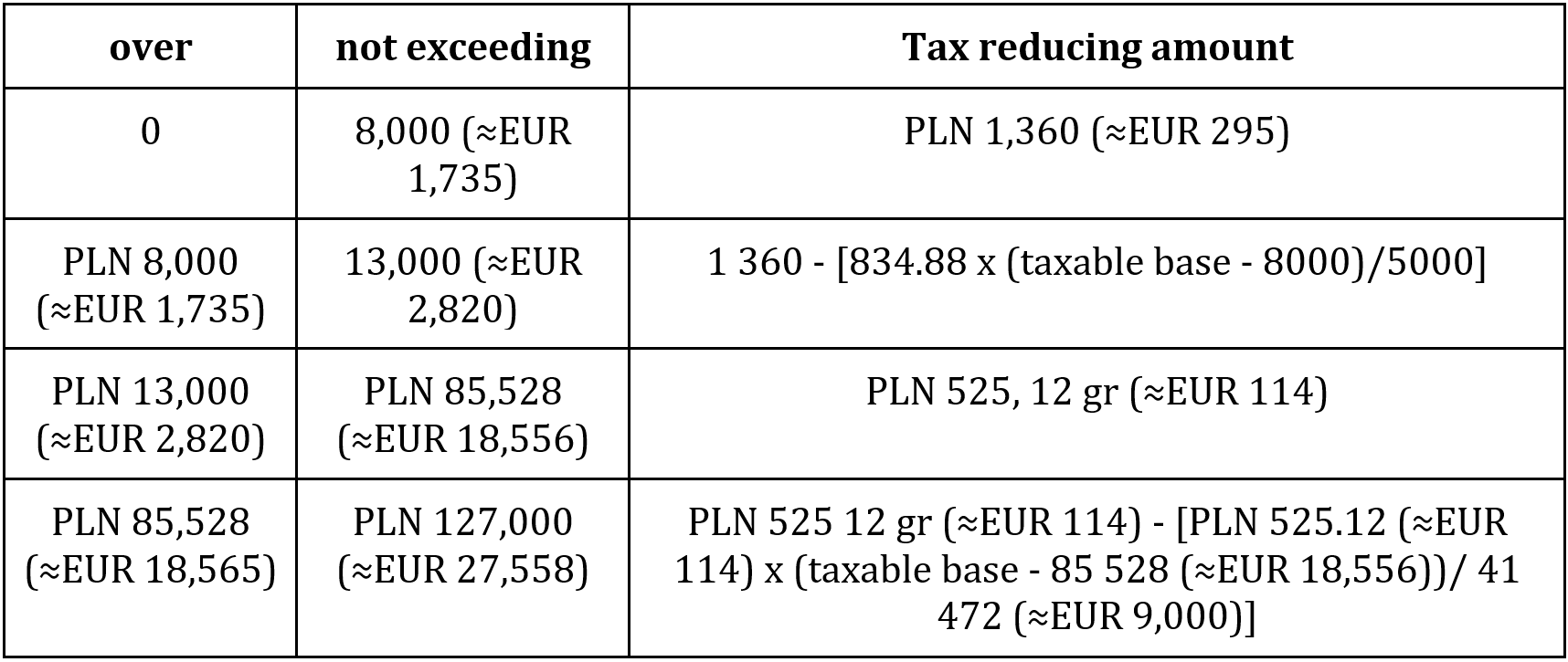

Tax-reducing amount, mentioned in the tax rate table above is deducted in the annual calculation of the tax and is estimated as following:

revenues from non-agricultural business activities are combined with other income from this source of income. Then the income (loss) on this account should be reflected in the tax declaration:

a) PIT-36, if the form of taxation has been chosen according to general principles, the income will be taxed according to the tax scale (above) as set out in article 27 of PIT;

There is no need to pay tax on cryptocurrencies throughout the year, in particular sales related taxes. Taxes related to cryptocurrency are settled only at the end of the year as shown in the annual declaration and only the annual tax on all settlements is paid.

Tax on civil law transactions

The contract for the sale and exchange of cryptocurrency, constitutes as property law, thus is subject to tax on civil law transactions. In conformity with article 7 of the PCC act, as regards sales contract, the obligation to pay this tax in the amount of 1% of the market value of the property right acquired in the cryptocurrency sold – applies to the buyer. In the case of an exchange agreement, the obligation to pay tax – in the amount of 1% of the market value of the property right, on which the higher tax is due – applies jointly and severally to the parties to the transaction.

Pursuant to art. 2 point 4 of the PCC Act, contracts for the sale or exchange of cryptocurrencies subject to value added tax (hereinafter:- “VAT”) are excluded from taxation of civil law transactions – to the extent that it is subject to VAT or if at least one of the parties to the transaction is exempt from VAT for this activity.

Value Added Tax

In line with article 8 of the Act on tax on goods and services, activities in the field of purchase and sale of virtual currencies are subject to VAT as a paid provision of services classified as electronic services, and therefore should be subject to VAT at the rate of 23%. However, for VAT purposes, the concept of currencies used as legal tender also includes the so-called cryptocurrency consistent with the norm Art. 43 sec. 1 point 7 of the VAT Act and CJEU judgment in Hedqvist C-264/14 case from October 2015. Meaning that, trading in virtual currency is exempt from this tax – in practice, anyone who receives income from trading in cryptocurrencies does not have to pay VAT, provided that the transaction is made in Poland.

This means that the sale and exchange of a cryptocurrency for traditional currency and vice versa, as well as the exchange of one cryptocurrency for another, as long as it is subject to VAT, benefits from a VAT exemption. Therefore, it should be remembered that, as a rule, the taxpayer does not have the right to deduct VAT on the purchased goods and services related to the mining and purchase / sale of cryptocurrencies. Tax liability in terms of VAT arises when the cryptocurrency is sold / exchanged for traditional currency, as well as when one cryptocurrency is exchanged for another.

The tax base (in accordance with the general rules on receiving remuneration from Article 29a (1) of the VAT Act) in the case of trading cryptocurrencies, both in terms of purchase / sale for traditional currency and for another cryptocurrency, is to be expressed in zlotys (PLN ).

Tax-deductible cost

Tax deductible costs are costs incurred in order to generate income or to maintain or secure a source of income. Such costs are therefore any expenditure which, collectively, meets the following conditions:

they were actually incurred in order to achieve income or to preserve or secure the source of income, i.e. they remain in a cause-and-effect relationship with the generated income;

have not been mentioned in Art. 23 of the PIT Act, containing a catalog of expenses not recognized as tax deductible costs;

are properly documented.

At the same time, it should be emphasized that in the case of cryptocurrency trading as part of business activities, the method of accounting and tax recording of the revenues and costs incurred depends on the type of tax books kept by the taxpayer (tax revenue and expense ledger or accounting books). It is worth noting that the tax revenue and expense ledger is a simplified and formalized form of recording economic events, therefore the taxpayer:

can make entries in it only on the basis of strictly defined documents listed in the Regulation of the Minister of Finance of August 26, 2003 on keeping the tax book of revenues and expenses, such as invoices or bills. Therefore, documents in the form of statements with the history of stock exchange transactions from the Internet cryptocurrency exchange, or bank statements with the history of transactions, do not constitute accounting evidence within the meaning of the provisions, and revenues and tax deductible costs documented only in this way cannot be recorded in the tax revenue and expense ledger.

Inability to record given revenues or expenses in the tax book of revenues and expenses – due to the fact that the taxpayer does not have the form of documenting them required in the regulation – does not automatically mean that they cannot be recognized as revenue and tax deductible costs, respectively, within the meaning of the PIT Act. Hence, if the taxpayer otherwise reliably documents the emergence of tax revenue or incurring the tax cost, it should be taken into account during the current tax year, as well as in the annual income tax settlement:

expenses for the purchase of cryptocurrencies are recognized in tax deductible costs at the time of incurring the expenditure, i.e. “on a regular basis”, i.e. on the date of purchase and according to the purchase price;

when settling the costs of obtaining revenues from cryptocurrency trading, there are no legal grounds for using the FIFO method (“first in – first out”) as referred to in Art. 30a paragraph. 3 of the PIT Act.

Other principles of accounting and documenting tax deductible costs apply to taxpayers who keep accounting books, in accordance with the provisions of the Accounting Act, because:

the provisions of the act do not contain a catalog of accounting documents that may constitute the basis for entries in the books of accounts, but only define its basic elements. For these reasons, e.g. bank statements confirming the cryptocurrency purchase or sale transactions along with the attached printout of the transaction made from the stock exchange profile of the unit, supplemented with the signature of the person who made the transaction on behalf of the unit, may be considered accounting evidence within the meaning of the Act;

there is a division of costs into indirect (deducted on the date they are incurred) and direct (deducted at the moment when the closely related revenue arises);

the provisions of the Accounting act allow the taxpayer to choose the FIFO method (“first in – first out”) to determine the value of the issue of certain goods.

Concluding remarks

Crypto assets are becoming a recognized participant in the contemporary financial market. Their increasing value ignites the interests of many investors. Although cryptocurrencies are not yet considered legal means of payment in Poland, officials already established sound regimes to tax transactions carried out using these currencies. Currently, acquisition and possession of digital currencies and keeping cryptocurrency accounts are not taxed, while the incomes derived from cryptocurrency trade are subject to taxation in Poland. Moreover, individuals must submit annual tax statements to declare revenues received from these assets. However, there are still some loopholes in the regulation of taxation, specifically: part of the employees salaries can be paid in virtual tokens, while the legislation doesn’t specify percentage of remuneration to be paid in cryptocurrencies and fiat currencies. The regulatory updates clearly confirm that the government endorses the usage of digital assets as substitutes of traditional banknotes, but the truth of the matter is that their use is not yet comprehensively regulated.

The content of this article is intended to provide a general guide to the subject matter, not to be considered as a legal consultation.

By clicking the "Contact us" button, I confirm that I have read the Privacy Policy and agree to the collection and processing of my personal data in accordance with the General Data Protection Regulation (GDPR).

Request Case Review

This site uses cookies to offer you a better browsing experience.