Despite the fact that India's population is really enthusiastic about virtual currencies, Indian laws do not yet control the usage of blockchain technology in business. At the same time, the Indian government has acknowledged blockchain as a critical and valuable technology, advocating for its implementation in the financial industry and other government areas.

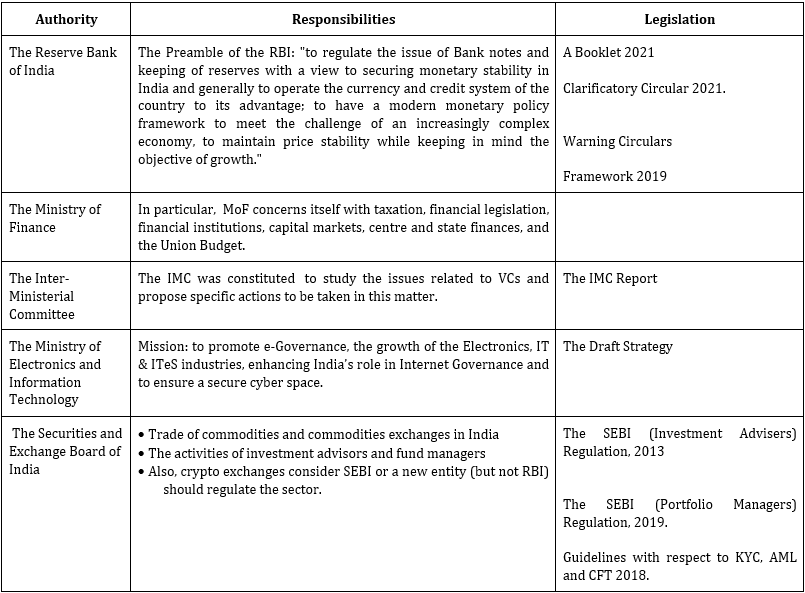

Since 2017, the Reserve Bank of India (hereinafter: “RBI“) has expressed significant worries regarding cryptocurrencies. RBI issued a circular in April 2018 (“Ring-Fencing Circular”) prohibiting any RBI-regulated entity from dealing in digital currencies or offering services that assist anyone in dealing with digital currencies. Money laundering, consumer protection, market integrity, cybersecurity, and volatility are among the concerns connected with virtual currencies, according to the RBI and the Ministry of Finance (“MoF”)(“Warning Circulars“).

Despite the government’s resistance to cryptocurrencies, India has taken a step closer to adopt digital currency after years of deliberation, as the country tries to stay up with the worldwide shift toward digital assets. In her budget statement, Finance Minister Nirmala Sitharaman stated that the RBI will introduce its central bank digital currency (hereinafter:- “CBDC”) on April 1, 2022. The country also intends to levy a 30% tax on profits derived from the transfer of virtual assets, essentially resolving any doubts regarding the legality of such transactions. The imposition of the tax rate makes crypto trade legal, and any fears of a ban are now immaterial.

Supervision

Legislative oversight

Despite the 2020 IAMAI case, which clarifies the legal nature of virtual currencies, no law exists today that categorizes virtual currencies as goods or services, securities, derivatives, or currencies.

As was mentioned earlier, in January 2021, the Ministry of Electronics and Information Technology (“MEIT”) introduced a National Strategy on Blockchain (“Draft Strategy”). This Draft Strategy identified regulatory gaps in the system as obstacles to widespread adoption of cryptocurrencies, and paid considerable attention to the following matters:

the ambiguous nature of tokens;

the lack of Know-Your-Customer (“KYC”) norms;

non-inclusion in the digital signature framework; and

adequate data protection provisions (including the right to be forgotten and localisation norms).

Individuals and legal entities may hold, invest in, and carry out transactions with cryptocurrencies as long as they follow all applicable laws. When dealing with cryptocurrencies, however, one must be aware of the recent amendment to Schedule III of the Corporations Act, 2013 (“CA Amendment“), which compels companies to disclose information. Furthermore, any bank or other RBI-regulated institution will be expected to perform appropriate due diligence procedures in compliance with existing laws and regulations. Companies in India are required to provide the following information under the amended Schedule III:

profit or loss on transactions involving cryptocurrency;

amount of currency held as at the reporting date; and

deposits or advances from any person for the purpose of trading or investing in cryptocurrency.

AML requirements

The RBI released an explanatory circular on May 31, 2021 (“Clarificatory Circular”) allowing regulated entities to transact cryptocurrency but adhering to existing KYC, AML, and CFT standards. While the Clarification Circular may only apply to regulated businesses, it is strongly advised that all entities, including those that provide cryptocurrency-related services (including crypto exchanges), comply with these duties. Know Your Customer (KYC) and anti-money laundering (AML) laws are currently enshrined in a variety of statutes and RBI instructions.

The KYC/AML standards set forth in various legislation (such as the Prevention of Money Laundering Act of 2002 and the RBI Know Your Customer (KYC) Directive of 2016) only apply to enterprises regulated by the RBI and other regulatory organizations such as SEBI. As a result, organizations working with security-related virtual currencies (as explained in Section II) or transactional payment systems (as discussed in Section III) may be subject to KYC/AML regulations.

The classification of tokens

In February of 2019, the Inter-Ministerial Committee published a Report to propose specific actions to be taken in relation to Virtual Currencies (“IMC Report”) in order to examine the problems with cryptocurrencies and to propose potential solutions. The Report provided a definition of “token” as “a utility, an asset or a unit of value issued by a company”, whose regulation may depend on the characteristics and the purpose for which they are issued. Tokens were further subdivided into “utility tokens” and “security tokens”.

Utility tokens: utility tokens offer investors access to a company‟s products or services. They are not to be treated as investment in a company.

Security tokens: security tokens represent investment in a company. Just like share-holders in a company, token holders are given dividends in the form of additional coins every time the company issuing the tokens earns a profit in the market.

Tax

In India, profits and earnings from the sale and trade of cryptocurrencies will be subject to taxation. As a result, the taxation of virtual currency-related activities can be divided into two categories: income tax (direct tax) and goods and services tax (GST) (indirect tax).

Direct tax: One of the critical questions under the ITA is whether income from virtual currencies is classified as capital gains or earnings and gains from a business or profession. At the moment, cryptocurrency has not been classified as an asset class or a good. Having said that, revenues and gains from the selling of cryptocurrencies are taxable in one of two ways:

the law in India recognises software as “goods” and income arising out of sale of software can be considered business income and be taxed as such (it will be taxable in India only if the non-resident has a permanent establishment in India);

the sale of any capital asset, in this case, cryptocurrency, would attract Capital Gains Tax (are typically taxed in India only if the asset is located in India).

GST: If cryptocurrency is classified as “goods,” every transaction will be taxed. In most circumstances, a vendor must charge the appropriate GST to the buyer/service recipient and deposit it with the revenue authorities. The parties to the transaction are also required to register as tax entities under the GST framework.

Conclusion

Considering everything, Indian regulators have chosen another vector of cryptocurrency regulation. It is reasonable to assume that the authorities have taken a firm position on cryptocurrencies, and that regulation in this field will be put in place soon.

By clicking the "Contact us" button, I confirm that I have read the Privacy Policy and agree to the collection and processing of my personal data in accordance with the General Data Protection Regulation (GDPR).

Request Case Review

This site uses cookies to offer you a better browsing experience.